' fill='%23419cd1'%3E%3Cpath d='m930.6-2156c-34.8 5.5-63.5 26.1-78.6 56.5-17.2 34.6-15 73.2 6.2 105.5 5.3 8.1 19.4 22.4 27.3 27.7 51.1 34.2 118.4 19.3 149.7-33.2 10.7-17.9 15.9-41.5 13.8-62.5-4.7-45.3-36-81.2-80.1-92-9.7-2.4-29.4-3.4-38.3-2z'/%3E%3Cpath d='m610.2-2094.9c-10.4 1.4-28 6-39.7 10.4-10.3 3.9-33.5 15-33.5 16.1 0 0.4 7.1 7.9 15.8 16.8 30.9 31.7 47.2 55.6 53.4 78.3 3.1 11.5 3.1 31.8 0 42.8-6.6 23.2-21.9 45.4-54.6 79.3-18.2 18.8-24.5 26.1-32.1 36.7-25.9 36.2-24 64.6 7 106 16.9 22.4 48.6 54 71.3 71 21.3 15.9 36.5 22.5 53.7 23.3 12.8 0.5 20.8-1.3 34-7.8 13.8-6.7 27.7-17.6 50-39 30.9-29.7 46.6-41.9 65.8-51 25.1-12 50.7-12.2 75.4-0.5 20.8 9.8 41.7 26.1 69.8 54.4 6.6 6.7 12.3 12.1 12.6 12.1 1.1 0 12.5-23.6 16.3-33.6 26.7-70.5 6.4-137.2-68.5-224.5-32.8-38.3-88.1-92.8-123.9-122-45.9-37.6-86.7-59.5-124.5-66.9-12.7-2.5-36.8-3.4-48.3-1.9z'/%3E%3Cg fill='%23efbd00'%3E%3Cpath d='m509.2-2050.1c-29 21.2-48.6 38.3-83.2 73-67.9 68-101.2 117.5-112.9 168.1-13.6 58.4 8.4 118.3 70.8 193 22.5 26.9 69.8 75.5 99.6 102.6 127.5 115.5 210.5 124.2 323.5 33.8 48.5-38.7 106.9-99.8 137-143.2l4.4-6.3-8.5-8.5c-12.1-12.4-33.6-32.3-41.5-38.6-35.1-27.8-61.5-32.7-92.2-16.9-14.1 7.3-28.1 18.3-51.6 40.7-23.9 22.7-32.6 30.2-44.9 38.5-38.5 25.8-73.7 25.3-114.2-1.7-35.5-23.7-82.1-72.5-100-105-16.5-29.7-17.4-56.9-3-85.9 9.3-18.7 17.1-28.5 51.9-65.2 8.7-9.3 19.3-21.4 23.5-27 30.5-40.6 29.2-70.6-5.2-113.3-9.6-11.9-41.3-45-43.1-44.9-0.6 0-5.3 3.1-10.4 6.8z'/%3E%3Cpath d='m339.2-1563c-22.6 3.2-44.4 14-60.3 29.9-31.4 31.4-39.4 78.7-19.9 118.6 13.4 27.6 37.8 47.7 67.8 55.7 9.9 2.6 31.2 3.5 42 1.8 35.6-5.7 67.5-31.3 80.3-64.4 6.5-16.9 8.9-39.2 5.9-55.7-8.8-48.6-49.6-84.4-98.4-86.3-6.1-0.3-13.9-0.1-17.4 0.4z'/%3E%3C/g%3E%3C/g%3E%3Cg fill='%23001522'%3E%3Cpath d='M7480.5 1379.2c-229 15-433 54-558 104-82 34-211 129-270 200-28 33-69 100-93 150-79 169-76 122-68 1035l7 810h191c105 0 211-5 236-11 60-14 103-49 131-106l24-48 10-1380 29-53c52-93 145-148 314-185 85-18 130-21 362-21 237 0 275 2 356 21 157 37 264 103 309 193 44 88 47 129 50 790 3 685 1 668 63 734 49 52 72 56 312 56h220l-2-838-3-837-26-63c-46-108-91-172-194-277-85-87-113-108-185-143-144-70-317-111-555-132-137-11-482-11-660 1zM11760 1378.2l-170 5-410 751c-225 412-425 773-443 802-46 70-134 150-176 157-70 14-149-47-234-179-26-40-222-402-437-804l-390-732h-282c-156 0-283 3-283 7s260 470 578 1037c562 1003 579 1032 649 1102 118 119 250 171 403 161 141-9 268-82 363-208 43-57 1197-2083 1197-2102 0-7-67-7-365 3zM13042 1376.2c-8 14 14 164 34 232 36 120 99 193 213 246 116 53 133 54 922 54 797 0 790 0 899 58 68 36 154 124 193 198 61 114 78 199 77 379 0 144-3 169-27 248-49 161-97 231-201 299-33 21-89 48-125 60-65 22-74 23-753 26l-688 3v-970l-36-7c-48-9-193 13-264 39-73 27-155 109-201 202l-34 70v475c0 435 2 479 18 528 24 68 60 110 117 135 44 20 67 21 905 24 473 3 935 0 1027-4l166-9 94-47c284-142 482-443 544-827 22-137 20-376-5-520-49-284-165-508-355-687-89-83-158-129-258-171l-63-27-500-6c-740-10-1693-10-1699-1zM17480 1382.2c-78 25-131 60-205 135-197 200-267 525-179 840 59 214 208 375 390 421 30 8 268 13 724 16 401 3 695 9 717 14 45 13 94 66 108 119 13 49-1 118-36 178-48 82 19 77-949 70l-860-7-55 32c-68 39-151 122-178 180-28 57-49 141-57 226l-7 69 137 6c228 11 2026 8 2086-3 186-35 341-210 406-458 21-81 25-119 25-232 0-163-20-250-88-389-59-120-155-220-259-272l-70-34-710-5c-689-5-711-6-744-25-19-11-45-40-59-65-20-37-23-55-19-105 5-74 37-139 80-165 30-19 53-19 858-13 759 6 831 5 871-10 55-21 94-61 153-157 57-93 84-181 87-285l3-80-385-6c-739-12-1741-9-1785 5z'/%3E%3Cuse xlink:href='%23i' width='100%25' height='100%25'/%3E%3Cuse xlink:href='%23i' width='100%25' height='100%25' transform='translate(6440.1)'/%3E%3Cuse xlink:href='%23i' width='100%25' height='100%25' transform='translate(10350)'/%3E%3C/g%3E%3C/svg%3E)

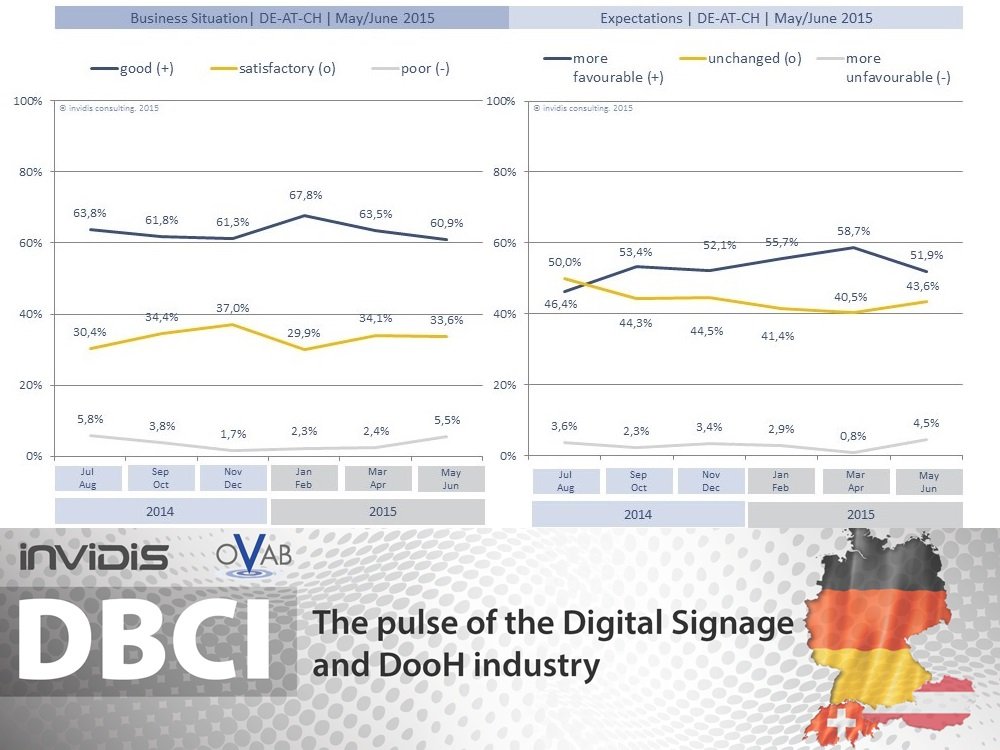

Since the last survey in March 2015 the Digital Signage Business Climate Index has declined slightly with a change of minus 8,20 base points from 59,50 base points to 53,35 base points. The current business situation has decreased slightly by 2 %. While the optimism towards the near future saw a more pronounced dip by 6 %.

After the traditionally good start into the new business year the Digital Signage market has seen a slight correction. The industry is expecting a similar low double digit growth for 2015 like in 2014. Moreover in Austria and Switzerland a shortage of skilled labour is an ongoing challenge for the IT industry, with no short term solution in sight.

Further research: Operating systems. Media Players and DooH challenges

MS Windows is still the dominant operating system for digital signage installations. However Linux is increasingly challenging Windows and Android records the highest dynamic.

External Media Player solutions dominate Digital Signage with 2/3 of all projects based on the Redmond-Platform. This option offers customers the highest variety from high performing industry PCs to low cost Android systems.

DooH market participants identified standardised audience measurement as the top challenge for their media. Even as association like OVAB Europe (in cooperation with DMI (DE) and IGDooH (CH) have or are in a process of introducing standardised measurement – acceptance on the media buyers side has still substantial upside potential.

The full survey of May/June 2015 can be downloaded here.